My Notes on Investments by Bodie

In this post, I share my notes from when I was reading the book Investments by Bodie ~2014. Please refer to the latest edition of the book for updated information.

-

Investments

-

Real Assets vs Financial Assets real assets and financial assets and how they contribute to the material wealth of a country. Real assets, such as land, buildings, machines, and knowledge, determine a country’s productive capacity and generate net income. On the other hand, financial assets, such as stocks and bonds, are merely securities that allow people to hold claims on real assets or income.

Individuals can choose to invest their wealth in financial assets by buying securities. Companies then use this money to purchase real assets and share the income with the investors. This means that the returns for investors come from the income generated by real assets.

There are three main types of financial assets: fixed income, equity, and derivatives. Fixed income securities, such as corporate bonds, promise a fixed stream of income, while equity, or common stock, represents a share in a corporation and its real assets. Derivatives, such as options or futures contracts, derive their value from the price of other assets, such as bonds or stocks. These securities are used to hedge risks or transfer them to other parties.

In addition to these financial assets, corporations regularly engage in currency transfers and investors can directly invest in real assets, such as commodities traded on exchanges. Firms also use commodities and derivatives to manage their exposure to business risks.

-

Financial Markets and the Economy

Financial markets play a crucial role in allocating capital in market economies through stock prices. The collective assessment of a firm’s current performance and future prospects reflected in stock prices can directly impact a firm’s ability to raise capital and encourage investment. Stock prices can also allow individuals to transfer purchasing power from their youth to older days by storing wealth in financial assets.

Diverse financial instruments in financial markets also allow investors with different risk tolerance to bear risk. For instance, a firm like Ford can raise funds through both stocks and bonds, with more risk-tolerant investors choosing to buy stocks and less risk-tolerant ones choosing bonds. This allows the inherent risk of the investment to be borne by those most willing to bear it.

The separation of ownership and management in large corporations also provides stability to the market. Ownership is distributed among a large group of individuals who elect a board of directors to manage the firm. However, there can be conflicts of interest between management and owners known as “agency problems.” To mitigate these issues, firms may tie executive compensation to the success of the company, have a board of directors that can force out underperforming management, and be subject to close monitoring by security analysts and institutional investors. Unhappy shareholders can also launch a proxy contest to elect a new board, or the firm may be at risk of takeover by other companies.

Transparency in the market is also crucial for informed decision-making by investors. The Sarbanes-Oxley Act of 2002 aimed to tighten rules of corporate governance and prevent misleading information. The act requires corporations to have more independent directors, tighter accounting standards, and increased oversight of public companies. These measures aim to promote ethical and responsible corporate behavior.

-

The Investment Process

The process of investing involves building a portfolio, a collection of investment assets, which can be updated over time by selling existing securities and using the proceeds to purchase new securities. Investors make two key decisions in constructing their portfolios: asset allocation and security selection.

Asset allocation involves deciding the proportion of one’s portfolio to allocate to different asset classes, such as stocks, bonds, or safe assets like bank accounts or money market securities. This decision is a crucial factor in determining the overall risk and return of the portfolio.

Security selection, on the other hand, involves choosing specific securities within each asset class to hold in the portfolio. This requires security analysis to determine the value of the individual securities.

There are two main approaches to portfolio construction: top-down and bottom-up. The top-down approach starts with the asset allocation decision and then moves on to security selection. The bottom-up approach focuses more on security selection and less on asset allocation, constructing the portfolio from securities that seem attractively priced.

-

Markets Are Competitive

Financial markets are constantly monitored by intelligent and well-funded analysts, meaning that there are no easy wins or “free lunches”. This idea has two important implications:

The Risk-Return Trade-Off: Investments come with a degree of risk and investors want to earn the highest returns they can. However, if an investment offers higher returns without taking on extra risk, many investors will jump on the opportunity, driving up the price and reducing the expected return. This means that there is a trade-off between risk and return in the securities market. Higher-risk assets offer higher expected returns, while lower-risk assets have lower expected returns.

Efficient Markets: The no-free-lunch proposition also implies that it’s rare to find bargains in the security markets. The financial markets process information about securities quickly and efficiently, meaning that security prices usually reflect all the information available to investors about their value. This is known as the efficient market hypothesis. If the markets are indeed efficient, it might be better to follow a passive investment strategy rather than trying to actively identify mispriced securities.

-

Financial Market Players

Financial markets are made up of three major players: firms, households, and governments. Firms need capital to fund their investments in plant and equipment and they raise this capital by issuing securities. Households, on the other hand, are the net suppliers of capital as they purchase these securities issued by firms. Governments can play both the role of borrowers and lenders, depending on their tax revenue and expenditures.

However, firms and governments do not sell their securities directly to the public. Instead, they hire financial intermediaries, such as banks, investment companies, insurance companies, and credit unions, to act as the go-between. Financial intermediaries issue their own securities to raise funds to purchase the securities of other corporations. They offer several advantages, including pooling the resources of many small investors, achieving significant diversification, and building expertise through the volume of business they do.

Investment bankers also play a crucial role in the financial market as they specialize in services for businesses, such as issuing securities, advising on prices and interest rates, and handling the marketing of securities in the primary market. Meanwhile, start-up companies rely on venture capital and private equity investments to fund their operations. These investments are usually made by dedicated venture capital funds, wealthy individuals known as angel investors, or institutions like pension funds.

-

-

Asset Classes and Financial Instruments

-

Money Market

The money market is a subsector of the fixed income market that includes highly marketable short-term debt securities. Many of these securities are traded in large denominations, making them unavailable to individual investors. To access these securities, investors can turn to mutual funds, which pool the resources of many individuals to purchase a diverse range of money market securities on their behalf.

-

T-bill

One of the most marketable money market instruments is the Treasury bill (T-bill), which is issued by the U.S government. T-bills are sold at a discount from their maturity value and provide a payment equal to the face value of the bill at maturity. They are issued with maturities of 4, 13, 26, and 52 weeks and can be purchased at auction or in the secondary market. T-bills are highly liquid, have little risk, and are usually denominated in $100, $10,000, or even $100,000. The income earned from T-bills is exempt from state and local taxes.

T-bills are typically quoted using the bank-discount method, which calculates the yield as a fraction of the face value and assumes a 360-day year. The bid price is the price at which a dealer is willing to purchase a T-bill, while the ask price is the price at which the T-bill is offered for sale. The difference between the bid and ask price is the bid-ask spread, which is the source of the dealer’s profit. The bond equivalent yield calculates the yield based on a 365-day year and is found by dividing the face value by the ask price and multiplying by 365/156.

-

Ceritficate of Deposti

A Certificate of Deposit (CD) is a fixed-term deposit with a bank. The investor cannot access the funds until the end of the specified term, at which point the bank pays both the interest and the principal value to the depositor. CDs are typically issued in denominations of $100,000 or more and are negotiable, meaning that the investor can sell the certificate before its maturity if necessary.

Short-term CDs are highly marketable and are easily sold, while longer-term CDs with a maturity of three months or more become less marketable. The Federal Deposit Insurance Corporation considers CDs to be bank deposits and insures them up to $250,000.

-

Commercial Paper

Companies that are well established often issue their own short-term debt notes, known as commercial papers, as an alternative to borrowing from banks. To ensure that they have the necessary funds to pay off the commercial paper at maturity, they may secure backing from a bank or a line of credit. The maturities of commercial papers typically range up to 270 days, with most maturities being less than 1 or 2 months and issued in multiples of $100,000. The Securities and Exchange Commission requires registration for maturities longer than 270 days, which is almost never done.

Individuals can invest in commercial papers through money market mutual funds. Because the firm’s performance can be monitored and predicted over a short term, such as 1 month, commercial papers are considered safe assets, often issued by nonfinancial firms. However, financial firms such as banks may issue asset-backed commercial papers to raise funds for investing in other assets, such as subprime mortgages. These assets were used as collateral for the commercial paper, which led to difficulties starting in 2007 when subprime mortgagors began defaulting and the banks were unable to issue new commercial paper to refinance their positions as the old paper matured.

-

Banker’s Acceptance

Banker’s Acceptance is a type of financial instrument in which a bank customer orders the bank to pay a specific amount at a future date, usually 6 months. The bank’s endorsement of the order signifies its responsibility for the ultimate payment to the holder of the acceptance. These instruments are often used in foreign trade to ensure payment when the creditworthiness of the counterparty is unknown. Upon endorsement, the Banker’s Acceptance can be traded in the secondary market. They are considered safe assets as they are backed by the credit of the bank rather than the borrower’s. Banker’s Acceptances are sold at a discount from the face value and are mostly used in international trade.

-

Eurodollars

Eurodollars are U.S. dollar-denominated deposits held in foreign branches of American banks. These banks are able to evade regulations imposed by the Federal Reserve by operating outside of its jurisdiction. Typically, Eurodollars are large deposits with short maturities of less than 6 months. Similar to domestic certificates of deposit, Eurodollar CDs are issued by a non-U.S. branch of a bank, usually located in London. Due to their lower liquidity and higher risk, Eurodollar CDs offer higher yields compared to domestic CDs. While Eurodollar bonds are also an option, they are excluded from the money market due to their longer maturities.

-

Repos and Reverses

Dealers in government securities often utilize repurchase agreements, also referred to as repos or RPs, as a short-term borrowing solution, typically for just one night. In a repo transaction, the dealer sells government securities to an investor at an agreed upon price, with a commitment to buy back the securities the next day at a slightly higher price, which represents the overnight interest. This operates similarly to a one-day loan from the investor, with the government securities serving as collateral.

For longer borrowing needs, a term repo operates in a similar manner, with the term of the loan lasting from 30 days or more. Repos are considered very secure as they are backed by government securities.

A reverse repo, on the other hand, is the opposite of a repo. In this transaction, the dealer buys securities from an investor, with an agreement to sell them back at a higher price in the future.

-

Federal Funds

The Federal Reserve System, also known as “the Fed,” is a network of banks that work together to ensure the stability and reliability of the US financial system. As part of this system, each member bank is required to maintain a minimum balance in a reserve account with the Fed. These funds in the bank’s reserve account are called “Federal funds” or “fed funds.”

At any given time, some banks may have more funds in their reserve accounts than required, while others may have a shortage. Big banks in New York tend to have a shortage of fed funds. In the Federal Funds market, banks with excess funds lend to those with a shortage. These loans are overnight transactions and are made at a rate of interest called the federal funds rate.

The fed funds was initially created as a way for banks to transfer balances to meet their reserve requirements. However, today, the market has evolved and many large banks use federal funds as a component of their sources of income. The fed funds rate is the rate of interest for short-term loans among institutions. Although most investors cannot participate in this market, the fed funds rate is still of great interest as it is seen as a key indicator of monetary policy.

-

Broker’s Call

Individuals who purchase stocks using margin borrow part of the funds from their broker. The broker may then borrow these funds from a bank, agreeing to repay the loan on demand if the bank requests it. The interest rate on these loans is typically 1% higher than the rate on short-term Treasury bills (T-bills).

-

The LIBOR Market:

The London Interbank Offered Rate (LIBOR) is a benchmark interest rate at which large banks in London are willing to lend money to one another. It is widely used as a reference rate in the money market and is tied to multiple currencies, including the US dollar. With trillions of dollars and various derivative assets tied to it, the LIBOR is a crucial reference rate in the financial industry.

-

Yiels on Money Market Instruments

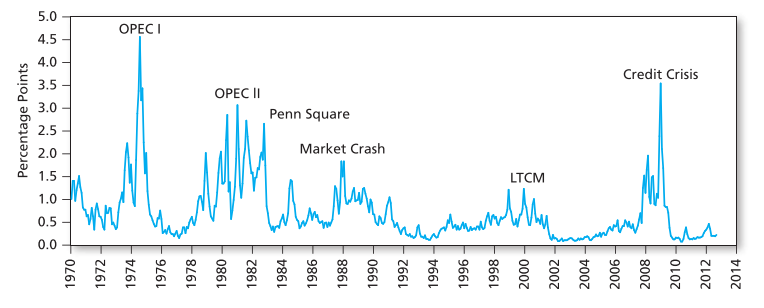

Most money market instruments are considered low-risk, but it’s important to note that they are not completely risk-free. While these securities typically offer yields higher than default-free T-Bills, investors usually prioritize liquidity, leading them to opt for lower yield options such as T-Bills. As shown in Figure 1, there is typically a gap between CD yields and T-Bills, and this gap widens during times of financial crisis. Similarly, the difference between LIBOR rates and T-Bills also increases during periods of financial stress.

-

-

-

The Bond Market

The bond market is a market for long-term debt instruments, as opposed to the short-term debt instruments found in the money market. The bond market includes Treasury notes, Treasury bonds, Corporate bonds, Municipal bonds, Mortgage securities, and federal agency debts. These debt instruments are often referred to as fixed-income capital market securities because they generally offer a fixed stream of income. However, in some cases, the formulas that determine the income stream may result in a flow of income that is far from fixed. As a result, it is more appropriate to refer to these securities as debt instruments or bonds.

-

Treasury Notes and Bonds

The U.S. government borrows money through the sale of Treasury Notes and Treasury Bonds. T-Notes have maturities of up to 10 years, while T-Bonds have maturities ranging from 1 to 30 years. They are usually quoted in denominations of $100 or $1000, with the latter being more common. Both T-Notes and T-Bonds make semiannual coupon payments, representing the interest earned on the investment.

An example of a T-Bill entry can be found in financial publications such as the Wall Street Journal, where its maturity date, coupon rate, bid price, asked price, change in price, and yield to maturity are displayed. The yield to maturity is calculated by determining the semiannual yield and then doubling it, instead of compounding it for two half-year periods. This results in an annual percentage rate (APR) rather than an effective annual yield.

It’s important to note that T-Bills are considered low-risk investments, but are not risk-free. The prices are quoted as a percentage of par-value, usually $1000, and can fluctuate based on market conditions.

-

Inflation-Protected Treasury Bonds

Many governments, including the U.S., offer bonds known as Inflation-Protected Treasury Bonds or TIPS as a way for citizens to hedge against inflation. These bonds are linked to the Consumer Price Index and their principal amount is adjusted accordingly. The yield on TIPS bonds represents real, inflation-adjusted rates and is a great starting point for building a low-risk investment portfolio.

-

Federal Agency Debt

Government agencies often issue their own securities to finance their operations, particularly in sectors that may not receive adequate credit through traditional private sources. Some of the major mortgage-related agencies include the Federal Home Loan Bank (FHLB), Federal National Mortgage Association (FNMA or Fannie Mae), Government National Mortgage Association (GNMA or Ginnie Mae), and the Federal Home Loan Mortgage Corporation (FHLMC or Freddie Mac). The FHLB, for example, raises funds by issuing securities and lending the money to savings and loan institutions, which then lend it to individuals for home mortgages. Although the debt of these federal agencies is not explicitly insured by the government, it was traditionally assumed that the government would assist an agency in the event of default. This assumption was validated in September 2008 when Fannie Mae and Freddie Mac experienced severe financial difficulties.

-

International Bonds

The international capital market, largely centered in London, provides opportunities for firms to borrow and for investors to purchase bonds from foreign issuers. A Eurobond is a bond denominated in a currency other than that of the country in which it is issued. For example, a bond denominated in dollars and sold in Britain would be considered a Eurobond. On the other hand, Yankee bonds are bonds issued by non-U.S. companies but denominated in dollars and sold in the U.S., while Samurai bonds are bonds issued by non-Japanese companies but denominated in yen and sold in Japan.

-

Municipal Bonds

Municipal bonds, also known as “munis,” are debt securities issued by state or local governments. They offer interest income that is exempt from federal and, in most cases, state and local taxes, making them attractive to many investors. There are two types of municipal bonds: General Obligation bonds, which are backed by the full faith and credit of the issuer, and Revenue Bonds, which are backed by the revenue from a specific project or agency.

Short-term Tax Anticipation Notes and long-term bonds are both available in the municipal bond market, with maturities ranging from a few months to 30 years. The tax-exempt status of municipal bonds is the main advantage that attracts investors, but to determine if they are a better investment option than taxable bonds, it’s important to consider an investor’s tax bracket and the equivalent taxable yield. The tax bracket at which an investor is indifferent between taxable and tax-exempt bonds can also be calculated by determining the yield ratio.

In general, the higher an investor’s tax bracket, the more attractive tax-exempt municipal bonds become. However, it’s important to consider the risk profile of the bond and the issuer’s creditworthiness before making any investment decisions.

The key feature of municipal bonds is their tax exemption status. Since investors are not paying any form of federal or local taxes, they are willing to accept lower rates on these securities.

How to compare between taxable and tax-exempt bond: let \(t\) denote the investor’s combined federal plus state tax bracket and \(r\) denote the total before tax rate of return available on taxable bond, then \(r(1-t)\) is the after-tax rate available on those securities. If this value exceeds the rate on municipal bond rate \(r_m\), then the investor does better holding the taxable bond. Another way to determine te interest rate on taxable bond that would be nevessary to provide an after-tax return equal to that of municipals. This value would be equal to \(r = r_m/(1-t)\). This is called equivalent taxable yield. Note that in order to find \(t\), a simple way is to add federal plus local tax rate together as \(t = t_{federal} + t_{state}\) . A more precise approach would recognize that the state taxes are deductible at the federal level. You owe federal taxes only on income net of state taxes. Therefore for every dollar of income, your after-tax proceeds would be \((1- t) (1-t_{federal})\times(1-t_{state})\). This way you could calculate combined federal and local taxes.

Note that the more your tax bracket is the more you are interested in holding municipal bonds that are tax-exempt. Because for every tax-exempt rate you need to get more yield for taxable yield.

Another, factor that can be computed is the tax bracket at which investors are indifferent between taxable and tax-exempt bonds. This bracket could be found as \(t = 1 - \frac{r_m}{r}\). The yield ratio, \(r_m/r\) is a key determinant of the attractiveness of municipal bonds. The higher the ratio, the lower the cutoff tax bracket, and then more individuals will prefer to hold municipal bonds.

-

Corporate Bonds

Corporate bonds are a type of debt securities issued by private companies to raise funds from the public. They work similarly to Treasury bonds, paying out semi-annual coupons and returning the face value to the bondholder at maturity. However, they are riskier than Treasury bonds due to the creditworthiness of the issuing company.

There are several types of corporate bonds, including secured bonds, which have specific collateral backing them in case of bankruptcy, unsecured bonds or debentures, which have no collateral, and subordinated debentures, which have a lower priority claim to the firm’s assets in the event of bankruptcy.

Additionally, some corporate bonds come with options attached. Callable bonds give the company the option to repurchase the bond from the holder at a predetermined price. Convertible bonds allow the bondholder to convert each bond into a specific number of shares of stock.

-

Mortgages and Mortgage-Backed Securities

Investing in mortgage-backed securities, which represent ownership or obligation claims in a pool of mortgages, has become a common aspect of the fixed-income market. Traditionally, these securities, also known as pass-throughs, were made up of conforming mortgages that met strict underwriting guidelines set by organizations such as Fannie Mae or Freddie Mac. However, in the lead up to the financial crisis, a significant amount of subprime mortgages were bundled and sold as mortgage-backed securities. These loans, made to financially weaker borrowers, were encouraged by the government to increase housing affordability for low-income households. However, they ended up causing huge losses, not just for banks, hedge funds and other investors, but also for Fannie Mae and Freddie Mac, which incurred billions of dollars in losses on the subprime mortgage pools they purchased.

-

-

Equity Securities

-

Common stocks

Common stocks, also known as equity securities or equities, represent ownership in a corporation. When you own a share of common stock, you are entitled to a vote in corporate governance matters and a share of the company’s financial benefits. Some corporations issue two classes of common stock, one with voting rights and one without. The one with restricted voting rights may sell at a lower price.

The corporation is governed by a board of directors elected by shareholders. The board meets several times a year to select managers who run the day-to-day operations of the company and ensure that it acts in the best interests of shareholders. Shareholders who cannot attend the annual meeting can vote by proxy, giving another party the power to vote on their behalf. Management typically solicits proxies from shareholders and typically receives a large majority of proxy votes.

There are several ways to make sure that management is following the goal of shareholders want, otherwise agency problems arises. There are several mechanisms that alleviate the agency problem, such (i) compensation schemes that link the success of the manager to that of the firm; (ii) oversight by the board of directors as well as outsiders such as security analysts, creditors, or large institutional investors; (ii) the threat of a proxy contest in which unhappy shareholders attempt to replace the current management team; or (iii) the threat of a takeover by another firm

The common stock of most large corporations can be bought and sold freely on one or more stock exchanges. A corporation whose stock is not publicly traded is said to be closely held. In most of closely held corporations, the owners of the firm also take an active role in its management. Therefore take overs are generally not a concern.

-

Characteristics of Common Stock

The two most important characteristics of common stock as an investment are (i) residual claim and limited liability.

Residual claim means that stock holders are the last ones in line among all those who have a claim on the assets and income of the corporation. In liquidation of the firm’s assets the shareholders have a claim to what is left after all other claims, such as tax authorities, employees, suppliers, bondholders, and other credits that have been paid. For a firm not in liquidation, shareholders have claim to the part of operating income left over after interest and taxes havebeen paid. Management can pay either pay this residual as cash dividends to the shareholders or reinvest in the business to increase the value of shares.

Limited liability means that the most shareholders can loose in the event of failure of the corporation is their original investment. Unlike owners of unincorporated businesses, whose creditors can lay claim to the personal assets of the owner (like house, car, or furniture), corporate shareholders may at worst have worthless stock. They are not personally liable for the firm’s obligation.

-

Stock Market Listings

The New York Stock Exchange (NYSE) is one of the platforms where investors can buy and sell stocks. A sample listing of a stock, such as General Electric (GE), might look like this:

- The closing price of GE stock is 19.72 dollars. - The net change from the previous trading day is +0.13 dollars. - On this day, 45.3 million shares of GE were traded. - The 52-week high and low prices of the stock are 21.00 dollars and 14.02 dollars, respectively. - The last quarterly dividend payment was 0.17 dollars per share (0.68 dollars divided by 4). - The annual dividend yield is 3.45%, calculated as 0.68 dollars divided by 19.62 dollars. - The price-earnings ratio is 16.01, which is the ratio of the current stock price to last year's earnings per share. - The stock has increased by 10.11% since the beginning of the year.It’s important to note that the dividend yield is part of the return on a stock investment. If a company pays a lower dividend, it’s expected to offer greater prospects for capital gains. The price-earnings ratio is a metric that tells us how much investors must pay for each dollar of earnings generated by the firm. A lower P/E ratio is generally seen as better.

-

-

Preferred Stock Preferred stock is a hybrid investment that combines features of both equity and debt. Like a bond, it offers a fixed, annual income payment and does not grant the holder voting rights in the management of the company. However, the company is not obligated to pay the preferred dividends and they are usually cumulative, meaning any unpaid dividends must be paid before common stock dividends are paid. On the other hand, the firm has a contractual obligation to make interest payments on its debt and failure to do so may result in bankruptcy proceedings.

The tax treatment of preferred stock is also different than bonds, as the payments are considered dividends instead of interest and are not tax-deductible for the company. However, corporations may exclude 70% of dividends received from domestic corporations when computing their taxable income, making preferred stock a desirable fixed-income investment for some corporations. For individual investors who cannot use the 70% tax exclusion, preferred stock yields may not be as attractive as other available assets.

Preferred stock can also be callable by the issuing company or convertible into common stock at a specified ratio. Adjustable-rate preferred stock links its dividend to current market interest rates, similar to adjustable-rate bonds.

-

Depository Receipts

American Depository Receipts (ADRs) are a convenient way for US investors to own shares in foreign companies. These certificates, traded in US markets, represent ownership in a foreign company’s shares. Each ADR can correspond to a fraction of a foreign share, one share, or multiple shares. ADRs were introduced to simplify the process of complying with US security registration requirements for foreign firms, making it easier for US investors to invest in international companies.

-

-

Stock and Bond Market Indexes

Stock Market Indexes are a measure of the overall performance of the stock market. The most well-known index is the Dow Jones Industrial Average, which tracks the performance of 30 large corporations. Additionally, there are foreign market indexes such as the Nikkei Average in Tokyo and the Financial Times Indexes in London, providing a glimpse into the performance of stock markets around the world.

-

Dow Jones Industrial Average

Aka DJIA is the average of 30 “blue-chip” corporations that is computed since 1896. DJIA covered only 20 stocks untill 1928 and then chaged to 30 stocks.

Originally, the DJIA was calculated as the average price of the stocks included in the index! Just adding the prices of these 30 stocks and dividing by 30. The percentage change in DJIA would then be the percentage change in the average price of the 30 shares. This means that the percentage change in DJIA measures the return (excluding dividends) on a portfolio that invests one share in each of the 30 stocks in the index. The value of such portfolio is the sum of the 30 prices (one share of each stock). Since the percentage change in the average of the 30 prices is the same as the percentage change in the sum, the index and the portfolio would have the same percentage change!

Since DJIA corresponds to a portfolio that holds one share of each component stock, the investment is proportional to the company’s share price! Therefore it is a price-weghted average.

The DJIA is now (Apr 2017) at a level of 20,000 and it is supposed to be average of only 30 stocks! Actually DJIA no longer equals to the average price of the 30 stocks, since the averaging procedure is adjusted whenever a stock splits or pay a stock dividend of more than 10%, or /when the company in the list is replaced by another firm/. When these events occur, the divisor used to compute the average is adjusted so to leave the index unaffected.

Company Exchange Symbol Industry Date Added 3M NYSE MMM Conglomerate 1976-08-09 American Express NYSE AXP Consumer finance 1982-08-30 Apple NASDAQ AAPL Consumer electronics 2015-03-19 Boeing NYSE BA Aerospace and defense 1987-03-12 Caterpillar NYSE CAT Construction and mining equipment 1991-05-06 Chevron NYSE CVX Oil & gas 2008-02-19 Cisco Systems NASDAQ CSCO Computer networking 2009-06-08 Coca-Cola NYSE KO Beverages 1987-03-12 DuPont NYSE DD Chemical industry 1935-11-20 ExxonMobil NYSE XOM Oil & gas 1928-10-01 General Electric NYSE GE Conglomerate 1907-11-07 Goldman Sachs NYSE GS Banking, Financial services 2013-09-20 The Home Depot NYSE HD Home improvement retailer 1999-11-01 IBM NYSE IBM Computers and technology 1979-06-29 Intel NASDAQ INTC Semiconductors 1999-11-01 Johnson & Johnson NYSE JNJ Pharmaceuticals 1997-03-17 JPMorgan Chase NYSE JPM Banking 1991-05-06 McDonald’s NYSE MCD Fast food 1985-10-30 Merck NYSE MRK Pharmaceuticals 1979-06-29 Microsoft NASDAQ MSFT Software 1999-11-01 Nike NYSE NKE Apparel 2013-09-20 Pfizer NYSE PFE Pharmaceuticals 2004-04-08 Procter & Gamble NYSE PG Consumer goods 1932-05-26 Travelers NYSE TRV Insurance 2009-06-08 UnitedHealth Group NYSE UNH Managed health care 2012-09-24 United Technologies NYSE UTX Conglomerate 1939-03-14 Verizon NYSE VZ Telecommunication 2004-04-08 Visa NYSE V Consumer banking 2013-09-20 Wal-Mart NYSE WMT Retail 1997-03-17 Walt Disney NYSE DIS Broadcasting and entertainment 1991-05-06 In order to better understand how DJIA works, lets suppose two stocks, ABC and XYS shwon in the following table. If we are introducing the DJIA for this table, the inital index and the final indexes are Initial Index Value \(= (25+100)/2 = 62.5\) and Final Index Value \(= (30+90) /2 = 60\). So at the end, we have Percentage Change \(= -2.5/62.5= -4\)%. Note that this does not represent the total market change, since the total market chages as Percentage Change in total market \(= \frac{690-600}{600} = +15\%\). This is because DJIA is price averaged, instead of the contribution that the stock is making to the market due to number of it shares in the market.

Stock Initial Price Final Price Shares Initial Value of Outstanding Stock Final Value of Outstanding Stock ABC $25 $30 20 m $500 m $600 m XYZ $100 $90 1 m $100 m $90 m Sum $600 m $690 m Now, suppose that the company XYZ splits it shares to two. The new values are shown in the following table. DJIA, will find a new divisor \(d\), such that the DJIA does not change afterward, as follows \begin{equation} \frac{\text{Price of ABS} + \text{Price of XYZ}}{d} = 62.5 \end{equation} Note that \(62.5\) is the initial DJIA that we had. The new devisor is then obtained as \(d = 1.2\). With this new divisor the final DJIA would be \((30 + 45)/1.2 = 62.5\), the same value at the start of the year. This would mean that the rate of return for such DJIA portfolio is zero. Note that still the whole market with these new values still have \(15\%\) return, if the portfolio was weigthed on the number of shares.

Stock Initial Price Final Price Shares Initial Value of Outstanding Stock Final Value of Outstanding Stock ABC $25 $30 20 m $500 m $600 m XYZ $50 $45 2 m $100 m $90 m Sum $600 m $690 m The same story happens when we replace a firm. The denominator is updated to leave the average unchanged. By 2017, the divisor of the DJIA has fallen to a value of \(0.146\). Since, DJIA is the average of small number of firms, representing the broad market, they change the composition every so often to reflect the changes in economy.

-

Standard & Poor’s Indexes* or S&P 500

The S&P 500 is a market-value-weighted index of 500 firms, which means that the weight of a firm in the index is proportional to its market value, calculated as the product of its stock price and number of shares outstanding. The index is computed daily by adding up the total market value of the 500 firms and comparing it to the total market value on the previous day of trading. An investment in the index is equivalent to holding a portfolio of all 500 firms in proportion to their market value, excluding cash dividends.

Most modern indexes use a modified version of market-value weights, known as free float market value, which only considers the value of shares that are freely available for investors to trade. This distinction is particularly important in Japan and Europe where a larger fraction of shares are held by non-tradable portfolios.

Both market-value-weighted and price-weighted indexes are straightforward to follow as investment strategies. A market-value-weighted index perfectly tracks the capital gain of a portfolio comprised of shares in each component firm in proportion to its market value. A price-weighted index tracks the returns of a portfolio comprised of an equal number of shares of each firm.

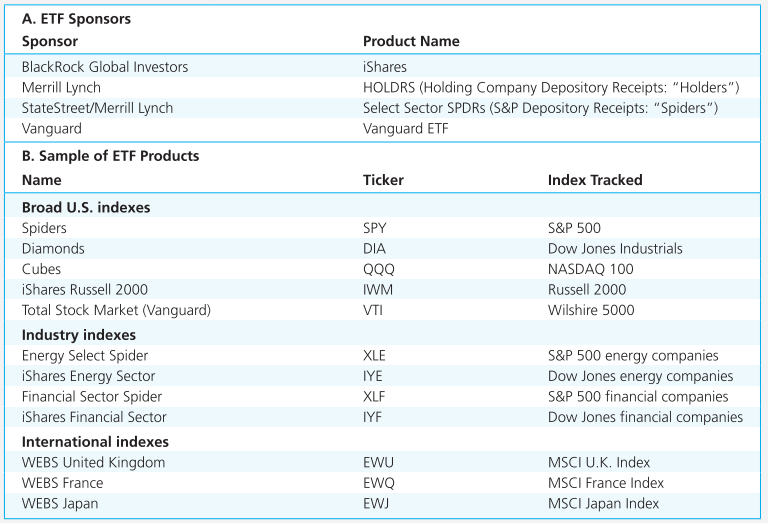

Investors can easily invest in market indexes by purchasing mutual funds or exchange-traded funds (ETFs). Index funds yield a return equal to the index, making them a low-cost investment strategy for equity investors. ETFs are portfolios of shares that can be bought and sold as a single unit, and there are a variety of ETFs available, from broad global market indexes to narrow industry indexes.

In addition to the S&P 500, Standard and Poor’s also publishes other stock indexes including the 400-stock Industrial Index, the 20-stock Transportation Index, the 40-stock Utility Index, and the 40-stock Financial Index.

-

Other U.S. Market-Value Indexes

The New York Stock Exchange (NYSE) publishes a composite index of all stocks listed on the NYSE, which is market-value weighted. This composite index includes subindexes for industrial, utility, transportation, and financial stocks. These indexes provide a broader view of the stock market than the S&P 500.

The National Association of Securities Dealers (NASD) publishes an index of more than 3,000 firms traded on the NASDAQ market.

The Wilshire 5000 index is considered the ultimate US equity index, as it tracks the market value of essentially all actively traded stocks in the US. It actually includes more than 5000 stocks. The performance of these indexes can be found in The Wall Street Journal.

-

Equally Weighted Indexes

Market performance can be measured using an equally-weighted average of the returns of each stock in an index. This averaging technique gives equal weight to each stock’s return, which corresponds to an implicit investment strategy of putting equal dollar amounts into each stock. This is different from both price weighting, which requires an equal number of shares of each stock, and market-value weighting, which requires investments in proportion to a stock’s outstanding value.

-

Foreign and International Stock Market Indexes

The growth of financial markets worldwide has led to the creation of indexes to track their performance. Some examples of these indexes include the Nikkei in Japan, the FTSE in the UK, the DAX in Germany, the Hang Seng in Hong Kong, and the TSX in Canada. Morgan Stanley Capital International (MSCI) is a leader in the creation of international indexes and calculates over 50 country indexes and several regional indexes.

-

Bond Market Indicators

Just as stock market indexes provide insight into the performance of the overall stock market, bond market indicators measure the performance of various categories of bonds. The three most well-known groups of bond market indexes are those of Merrill Lynch, Barclays (previously the Lehman Brothers index), and Salomon Smith Barney (now part of Citigroup).

However, there is a major challenge with bond market indexes: accurately computing the true rates of return on many bonds. This is because the infrequency of bond trades makes it difficult to obtain reliable, up-to-date prices. As a result, some prices must be estimated using bond valuation models, which may not reflect the true market values.

-

Derivative Markets

The derivative market consists of two main instruments: futures and options. These financial instruments provide payouts that are based on the values of underlying assets, such as commodity prices, bond and stock prices, or market index values. Because the value of these instruments depends on the value of other assets, they are referred to as derivative assets.

-

Options

A call option gives its holder the right to purchase an asset, such as stock, at a specified exercise price, also known as the strike price, before or on a specified expiration date. For example, a July call option on IBM stock with an exercise price of $180 allows the holder to buy IBM stock for $180 at any time until the expiration date in July. Each option contract covers the purchase of 100 shares, but quotations are made on a per-share basis. The holder of the call option does not have to exercise it, and it will only be profitable to do so if the market value of the asset is higher than the exercise price. When the market price exceeds the exercise price, the option holder can “call away” the asset for the exercise price and receive a payoff equal to the difference between the stock price and the exercise price. If not exercised before the expiration date, the option simply expires and becomes worthless. Call options are bullish investment vehicles that provide greater profits when stock prices increase.

In contrast, a put option gives its holder the right to sell an asset for a specified exercise price before or on a specified expiration date. For example, a July put option on IBM with an exercise price of $180 allows the holder to sell IBM stock for $180 to the put writer at any time before the expiration date in July, even if the market price of IBM is lower than $180. Profits on put options increase when the asset decreases in value, unlike call options that benefit from an increase in the asset’s value. The put option is exercised only if its holder can deliver an asset worth less than the exercise price in return for the exercise price.

It is important to note that the price of a call option decreases as the exercise price increases. For instance, a call option for May 5, 2017 with an exercise price of $144 is only $3.13. This makes sense because the right to purchase a share at a higher price is less valuable.

On the other hand, the price of a put option increases with the exercise price. For example, the right to sell APPL shares for $130 is $0.31, while the right to sell shares for $143 is $3.07.

Another factor that affects option prices is the expiration date. Option prices increase as the expiration date approaches. For instance, a call option for $130 a share is worth $17.75 if the expiration date is in November, compared to $13.10 if the expiration date is in May.

-

Future Contracts

A futures contract requires delivery of an asset (or its cash value) on a specified delivery or maturity date, for an agreed-upon price, called the futures price, to be paid at contract maturity.

The trader who holds the long position commits to purchasing the asset on the delivery date, while the trader who takes the short position commits to delivering the asset at contract maturity.

Table 8 shows some futures contracts for crude Brent oil listed on the Chicago Mercantile Exchange. Each contract calls for delivery of 1,000 barrels of oil. The table lists the prices for contracts expiring on various dates, with the first row being the nearest or front contract with a maturity date of June 2017. For example, the most recent price was $54.89 per barrel, an increase of $0.3 from the previous day’s close. The table also shows the opening price, as well as the high and low prices for the trading day. The volume column shows the number of contracts traded that day, but there is no column for “Open Interest” which represents the number of outstanding contracts.

Month Last Change Prior Settle Open High Low Volume JUN 2017 55.19 0.3 54.89 54.75 56.07 54.57 33006 JUL 2017 55.55 0.38 55.17 55.08 56.23 54.86 12892 AUG 2017 55.64 0.29 55.35 55.37 56.46 55.15 7571 SEP 2017 55.65 0.2 55.45 56.2 56.27 55.45 6660 The trader holding the long position in a futures contract profits from price increases. For example, if at contract maturity, the price of oil is $55.50 per barrel and the trader entered the contract at a future price of $55.19 per barrel on June 2017, they would pay the agreed-upon price of $55.19 for each barrel of Brent oil, which would then cost $55.50 at contract maturity. In this case, the profit for the long position would be $2100 (1000 x ($55.50 - $55.19)). Conversely, the short position trader must deliver 1,000 barrels at the previously agreed-upon futures price, and their loss would equal the long position trader’s profit.

The key difference between a call option and a long position in a futures contract is the obligation to purchase the asset. While a futures contract obliges the long position trader to purchase the asset at the futures price, a call option conveys the right to purchase the asset at the exercise price. A call option holder has a better position than the holder of a long position in a futures contract with a futures price equal to the option’s exercise price, but this advantage comes at a cost. Call options must be purchased, whereas futures contracts are entered into without cost. The purchase price of an option, called the premium, represents the compensation the call option holder must pay for the ability to exercise the option only when it is profitable to do so. Similarly, the difference between a put option and a short futures position is the right, as opposed to the obligation, to sell an asset at an agreed-upon price.

-

-

-

How Securities are Traded

-

How Firms Issue Securities

Firms need capital to finance their investments, which they can raise by either borrowing money or selling shares. Investment bankers are hired to handle the sale of these securities in the primary market, where newly issued securities are sold to the public. After the initial sale, investors can trade their shares of existing securities in the secondary market.

Publicly listed firms’ shares can be continuously traded on well-known stock markets such as the New York Stock Exchange (NYSE) or NASDAQ Stock Market. Any investor can purchase shares for their own portfolio from these markets. Companies traded on these markets are referred to as publicly traded, publicly owned, or simply public companies. In contrast, private corporations have shares that are held by a small group of managers and investors.

-

Privately Held Firms

A privately held company is owned by a relatively small group of shareholders, who are not required to publicly disclose financial statements and other information as frequently as publicly traded companies. This allows the company to pursue long-term goals without the pressure of quarterly earnings announcements.

However, private companies are limited to having up to 499 shareholders, which restricts their ability to raise large amounts of capital. To overcome this restriction, middlemen may form partnerships to buy shares in private companies, which counts as only one investor even though many individuals may participate.

When a private company needs to raise funds, it sells shares directly to a small number of institutional or wealthy investors in a private placement. The SEC’s Rule 144A allows these companies to make these placements without having to prepare extensive and costly registration statements. Although attractive, shares of privately held companies do not trade in secondary markets such as the NYSE or NASDAQ Stock Exchange, reducing their liquidity and presumably lowering their prices.

Recently, some firms have set up computer networks to enable private company stockholders to trade among themselves. However, unlike public stock exchanges regulated by the SEC, these networks require little disclosure of financial information and provide limited oversight of the market operations.

-

Publicly Traded Companies

When a private firm wants to raise capital from a wide range of investors, it may choose to go public by selling its securities to the general public and allowing them to freely trade shares in the established securities market. The first sale of shares to the public is called an Initial Public Offering (IPO). Later, the firm may issue more shares through a seasoned equity offering.

Investment bankers are responsible for marketing public offerings of both stocks and bonds and are often referred to as underwriters. More than one investment banker may be involved in marketing the security, with a lead firm forming a syndicate of other investment bankers to share the responsibility of the stock issue.

The investment bankers advise the firm on the terms of the sale and help prepare a preliminary registration statement that is filed with the Securities and Exchange Commission (SEC) to describe the issue and the prospects of the company. When the statement is in final form and accepted by the SEC, it is called a prospectus, and the price at which the securities will be offered to the public is announced.

In a typical underwriting arrangement, the investment bankers purchase the securities from the issuing company and then resell them to the public. The issuing firm sells the securities to the underwriting syndicate for the public offering price, less a spread that serves as compensation for the underwriters. In addition to the spread, investment bankers may also receive shares of common stock or other securities from the firm.

-

Shelf Registration

In 1982, the SEC approved Rule 415, which enables firms to register securities and gradually sell them to the public over a period of 2 years after the initial registration. As the securities are registered, they can be sold quickly with limited additional documentation. These securities are referred to as “on the shelf” and ready for issuance, which gave rise to the term “shelf registration.

-

Initial Public Offering

Investment bankers play a crucial role in the process of issuing new securities to the public. They coordinate road shows to generate interest among potential investors and gather information about the demand and prospects of the security. The underwriters use the information gathered from these road shows, along with feedback from institutional investors, to determine the offering price and number of shares to be offered.

Investors communicate their interest in purchasing shares of the IPO to the investment bankers through a process called book building. The allocation of shares to investors is partially based on the strength of their expressed interest in the offering. This creates an incentive for investors to truthfully reveal their interest, as underpriced IPOs often result in significant price jumps on the first day of trading.

However, while IPOs often offer attractive first-day returns, they have been poor long-term investments on average. According to research by Ritter, a portfolio of equal amounts of each U.S. IPO between 1980 and 2009, held for three years, would have underperformed the broad U.S. stock market by 19.8%. The 2011 IPO of Groupon is an example of underpricing, while the IPO of Facebook is an example of overpricing.

-

-

How Securities are Traded?

-

Types of Markets

-

There are four types of markets: 1) Direct search markets 2) Brokered Markets 3) Dealer Markets 4) Auction Markets

-

Direct Search Markets: are the least organized markets. Buyers and sellers seek each other out directly. An example of a transaction in such markets is the sale of a used TV on craigslist where the seller advertises for buyers in local area. These markets are characterized by sporadic participation (meaning scattered), low-priced and non-standard goods. Firms find it difficult to profit in a such environment.

-

Brokered Markets: are the next level of organization. Brokers offer search serives to buyers and sellers, in markets where trading a good is active. An example, is real state market, where buyers make it worthwhile for participants to pay broker to help them conduct the search. Another example, is the primary market where new issues of securities are offered to the public. Investment bankers act as brokers as they seek investors to purchase securities directly from the issuing corporation.

-

Dealers Market: When trading activity increases in a particular type of asset, then dealer markets arise. Dealers specialized in various assets, buy these assets for their own, and later sell them for a profit from their inventory. The spread between dealer’s buy (or “bid”) and sell (or “ask”) prices are a source of profit They save traders the search costst, because one can easily look up their prices. An example is the “second hand car dealers”. Also most bonds trade in over-the-counter dealer markets.

-

Auction Markets: The most integrated market is an auction market, where traders converge at on eplace (either “physically” or “electronically”) to buy and sell asset. An example of such markets is New York Stock Exchange (NYSE). An advantage of auction markets to dealer markets is that one need not search across dealers to find the best price for a good. If all participants converge, they can arrive at mutually agreeble prices and save the bid-ask spread.

-

-

Types of Orders

There are different types of trades an investor is eager to execute in these markets. Broadly speaking we have two types of orders: (i) Market orders and (ii) Price Contingetn Orders.

-

Market Orders

Market orders are buy or sell orders that are to be executed immediately. For example, an investor might call his broker and ask for the market price of APPL. The broker will reort back that the best bid price is 140$ (the price to buy shares) and the best ask price is 141$ (the price to buy shares). The bid-ask spread in this case is 1$.

There are several complications here: First, the posted price quote actually represent commitments to trade up to a secific number of shares. If the market order is more than this number of shares, multiple may be filled at multiple prices. For example, if the investor wants to buy 1,500 shares and the ask price is good for 1,000 shares, it may be necessary to pay a slightly higher price for the last 500 shares. The depth of the markets for shares of stock, shows the total number of shares offered for trading at each bid and ask price. Depth is considered a component of liquitidty. Second, another trader may beat the investor to the quote, this means that the investor’s order would then be executed at a worse price. Third and finally, the best price quote might change before the order arrives, causing execution at a price different from the one at the moment of order.

-

Price Contingent Orders

Investors may also place orders specifying prices at which they are willing to buy or sell a security.

A limit-buy order instructs the broker to buy some number of shares if the stock price may be obtained at or below a stipulated price.

Conversely, limit-sell order instructs the broker to sell if and when the stock price rises above a specified limit.

limit-order book is a collection of limit-orders to be executed. The best orders are at the top of the list. Offers to buy at the highest price, and offers to sell at the lowest price. The buy and sell orders at the top of the list are called inside quotes. The order sizes for the inside quotes can be fairly small. Therefore, investors interested in larger trades face an effective spread greater than the nominal one because they cannot execute their entire trade at the inside quote.

Stop-orders are similar to limit orders in that the trade is not to be executed unless the stock price hits a limit. For Stop-loss orders, the stock is to be sold if its price falls below a stipulated price. As the name suggests, this order is executed to stop furthe loss accumulation. Similarly Stop-buy orders specify a stock should be bought when the its rice rises above a limit.

These stop orders often accompany short sales (sales of securities when you don’t own but have borrowed from your broker) and are used to limit potential losses from short position.

All these price contingent orders all together

Price Below the limit Price above the limit Buy limit-Buy Order Stop-buy order Sell Stop-loss order limit-sell order

-

-

Trading Mechanisms

An investor who wants to buy or sell stocks, will ask the broker. The broker charges a commission fee for arranging the trade on client’s behalf. Brokers have several options, to execute the trade.

There are three trading systems used in the US: * over the counter dealer markets * electronic communication networks * specialist markets

NASDAQ and NYSE are the best well known markets. They use a variety of trading procedures.

-

Dealers Market

Roughly 35,000 securities trade on over-the-counter or OTC markets. Thousands of brokers register with SEC as security dealers. Dealers quote prices they are willing to buy or sell. Then they contact a dealer listing an attractive quote and execute the trade.

Before 1971, OTC quotions were recorded manually and published daily on so called pink-sheets. In 1971, the National Association of Securities Dealers introduced Automatic Quotions System, or NASDAQ, to link brokers an dealers in a computer network, to displayrevise quotes on the network. Dealers used this system to post their bidask pric. The difference between bid and ask price, the bid-ask spread, is the source of dealer’s profit. Dealers examine prices online and then contact the delaer with the best quote and execute a trade.

The NASDAQ as was originally desinged, was more of a price quotion system to post bid/ask prices. Brokers in the search of best trading opportunity, would contact the dealer and directly negotioate over the phone. NASDAQ Stock Market has now been added to NASDAQ and it allows for electronic execution of trades.

-

Electronic Communivation Network (ECNs)

ECN allows participants to post market limit orders over the computer networks. The limit order book is available for all of the participants. NYSE Arca is one of the leading ECNs. Orders are crossed, when they match on the limit-order book, without intervention of a broker. Therefore, ECNs are true trading systems, not merely price quotion systems.

ECNs have several benefits: (i) Direct and automatic crossing without using a broker-dealer system (ii) Modest cost trades typically less than a penny per share, since they are automatic, (ii) elimination of bid-ask spread, since trades are crossed automatically, (iv) Fast speed at which trades are done, and (v) anonymity in the trades

-

Specialist Markets

This has been largely replaced by electronic communication networks. A decade ago, they were dominant form of market organization for rading stocks. In thi system, exchanges such as NYSE assign representativesfor managing the trade in each security to a specialist. Brokers wishing to buy/sell trades would contact the specialist on board of exchange. The specialist would manage all of the order book.The highest bid, and the lowest ask price would win the trade.

-

-

-

The Rise of Electronic Trading

The NASDAQ and NYSE stock markets have undergone significant changes in the past few decades, transitioning from over-the-counter dealer markets and specialist markets to primarily electronic markets. Advances in technology and new regulations have brought about these changes. Regulations allowed brokers to compete for business, breaking their hold on information and reducing price increments. The integration of markets and the availability of technology to rapidly compare prices across markets has also reduced the cost of trade execution.

In 1975, the fixed commission on the NYSE was eliminated and the Securities and Exchange Act was amended to create the National Market System, which aimed to partially centralize trading across exchanges and enhance competition. The implementation of a centralized reporting of transactions and price quotation system provided traders with a broader view of market opportunities.

In 1994, a scandal at the NASDAQ involving dealers colluding to maintain wide bid-ask spreads led to the SEC instituting new order-handling rules. Published dealer quotes were now required to reflect customer limit orders and NASDAQ agreed to integrate quotes from electronic communications networks (ECNs) into its public display. This allowed ECNs to compete for trades and led to the SEC adopting Alternative Trading System Regulations, which gave ECNs the right to register as stock exchanges.

The SEC has continued to reduce the minimum tick size, which has resulted in a reduction of bid-ask spreads. In the 1990s, exchanges around the world began adopting electronic trading systems and the NASDAQ Stock Market was established as a separate entity. In 2006, the NYSE acquired the electronic Archipelago Exchange and renamed it the NYSE Arca. In 2007, the SEC fully implemented Regulation NMS, which required exchanges to honor quotes from other exchanges when they could be executed automatically.

Today, trading is almost exclusively electronic for stocks, with bonds still being traded in traditional dealer markets.

-

U.S. Markets

The NYSE and NASDAQ Stock Market are the two largest US stock markets. But other ECNs (namely BATS, NYSE Arca, Direct Edge,…) have steadily increased their market share.

-

NASDAQ

The NASDAQ Stock Market lists 3,000 firms and its trading platform has improved over the years. Currently, the NASDAQ Market Center integrates NASDAQ’s previous electronic markets into a single system.

In 2008, NASDAQ merged with OMX, a Swedish-Finnish company that controls seven Nordic and Baltic stock exchanges, to form NASDAQ OMX Group. This group manages not only the NASDAQ Stock Market, but also several stock markets in Europe, as well as options and futures exchanges in the US.

NASDAQ has three levels of subscribers:

-

Level 3: The highest level of registered market makers. These firms create a market in securities, maintain inventories of securities, and post bid and ask prices at which they are willing to buy or sell shares. They can continuously enter and change bid-ask quotes and have the fastest execution of trades. They profit from the spread between bid and ask prices.

-

Level 2: Receive all bid and ask quotes but cannot enter their own quotes. They can see which market makers are offering the best bid and ask prices. They are usually brokerage firms that execute trades for their clients but do not actively deal in stocks for their own account.

-

Level 1: Receive only inside quotes, i.e., the best bid and ask prices, but do not see the number of shares being offered. They are usually investors who are not actively buying or selling, but want information on current prices.

-

-

NYSE

The NYSE (New York Stock Exchange) is the largest stock exchange in the US, measured by the value of stocks listed on the exchange. On a daily basis, the NYSE has a trading volume of approximately one billion shares.

In 2006, the NYSE merged with Archipelago Exchange to form NYSE Group, a publicly-held company. In 2007, NYSE Group merged with Euronet to form NYSE Euronext. In 2008, NYSE Euronext acquired the American Stock Exchange, which was then renamed as NYSE Amex to focus on smaller firms. NYSE Arca is the firm’s electronic communication network, where the majority of exchange-traded funds are traded. In 2012, NYSE Euronext was acquired by International Exchange (ICE), a company primarily focused on energy-future trading. ICE plans to retain the NYSE Euronext name and the iconic trading floor on Wall Street.

The NYSE has many trading specialists who rely heavily on human involvement in trade execution. The exchange began its transition to electronic trading in 1976 with the introduction of DOT (Designated Order Turnaround) and later the SuperDOT system, which routes orders directly to specialists. In 2000, the NYSE launched Direct+, which allowed for automatic cross of smaller trades (up to 1,099 shares) without human interaction. In 2004, Direct+ began eliminating the transaction size limit. The transition to electronic trading accelerated in 2006 with the introduction of the NYSE Hybrid Market, which allowed brokers to send orders for either immediate electronic execution or to a specialist for price improvement. The Hybrid System allowed the NYSE to remain as a fast market for purposes of Regulation NMS while still offering the benefits of human intervention for more complex trades. Note that NYSE Arca is fully electronic.

-

ECNs

Over time, automated markets have gained a larger market share. Today, some of the largest ECNs include BATS, Direct Edge, and NYSE Arca. Brokers affiliated with an ECN have computer access and can enter orders into the limit order book. When orders are received, if a matching trade is found, the trade is immediately executed.

Initially, ECNs were only open to traders using the same system. However, after the implementation of Regulation NMS, ECNs started to list limit orders on other networks.

These cross-market links have paved the way for more popular strategies, such as high-frequency trading, which aim to profit from even small price differences across the market. Speed is critical in these strategies, and ECNs compete based on the speed they can offer. Latency refers to the time it takes to accept, process, and execute a trading order. For example, BATS advertises latency times of around 200 milliseconds.

-

-

New Trading Strategies

Electronic trading has introduced new opportunities for various trading strategies and tools. One such strategy is algorithmic trading, where the trading decisions are handed over to computer programs. Another type of algorithmic trading is high frequency trading, which involves the use of computer programs to initiate trades in a matter of milliseconds, much faster than a human could process. This type of trading brings a large amount of liquidity to the market, but it can also lead to a rapid withdrawal of liquidity, as seen in the flash crash of 2010. Dark pools are another aspect of electronic trading, where the trading takes place in an anonymous manner, but it can have an impact on market liquidity.

-

Algorithmic Trading

Algorithmic Trading” involves using computer programs to make trading decisions. It is estimated that more than half of all equities traded in the US are initiated by algorithms. These strategies were made possible by the decimalization of the minimum tick size.

There are different types of algorithmic trading, including exploiting short-term trends, pair trading to take advantage of temporary disruptions in the normal price relationship between stocks, and exploiting discrepancies between stock prices and stock index future contract prices.

Some algorithms aim to profit from the bid-ask spread by quickly buying a stock at the bid price and selling it at the ask price before the price changes.

-

High Speed Frequency Trading

Algorithmic trading strategies often require extremely fast trade initiation and execution, and high-frequency trading is a subset of algorithmic trading that uses computer programs to make rapid decisions. These trades compete for opportunities that offer small profits, but they can add up to significant amounts.

Some algorithmic strategies profit from the bid-ask spread, while others rely on cross-market arbitrage, taking advantage of even tiny price differences across markets. The firms that are quickest to identify and execute these trades win the profits. Today, trade execution times for high-frequency trades are measured in milliseconds or even microseconds, and firms are locating their trading centers near electronic exchange centers for faster access.

The location of trading centers has become crucial in this high-speed competition. A trade order originated in Chicago, for example, takes 5 milliseconds to reach New York. During this time, another firm located in New York could win the trade. ECNs today claim latency periods of 1 millisecond.

-

Dark Pools

Many big traders prefer to remain anonymous when buying or selling large amounts of stocks as the public knowing about their transactions can affect the stock prices.

Traditionally, large trades (known as “Blocks” with more than 10,000 shares) were handled by “block houses,” which are brokerage firms that specialize in matching buyers and sellers of large blocks. These brokerages execute trades privately, avoiding price movements against their clients.

However, block trades have now been replaced by “Dark Pools,” which are trading systems where participants can buy or sell large blocks of securities without revealing their identities or the details of the trades. This contributes to the fragmentation of the markets, as fewer orders are visible on consolidated limit order books, potentially leading to an unfair public price that does not reflect all available information about the security demand.

Another approach to dealing with large trades is to divide them into smaller trades, which can be executed on electronic markets, thereby hiding the fact that a large amount of shares have been bought or sold. This has led to a rapid decline in the average trade size, which is now around 300 shares.

-

Bond Trading

In 2006, the NYSE gained regulatory approval to list debt issues from any NYSE-listed company on its bond-trading system. This made it easier for bonds to be listed and resulted in the expansion of NYSE’s electronic bond-trading platform, now known as NYSE Bonds, which is now the largest centralized bond market in the US.

It’s important to note that the majority of bond trading still takes place in the over-the-counter (OTC) market among bond dealers, even for bonds listed on the NYSE. Major players in the bond market include Merrill Lynch (now part of Bank of America), Salomon Smith Barney (a division of Citigroup), and Goldman Sachs.

However, the bond market also has liquidity risks, which can make it difficult to sell holdings quickly if necessary.

-

-

Flash Crash of May 2010

On May 6, 2010, the Dow Jones Industrial average experienced a rapid drop in value. At 2:42 PM New York time, the market was down by approximately 300 points due to concerns about the European debt crisis. However, within the next five minutes, the Dow plummeted an additional 600 points. After 20 minutes, it regained most of those losses. This sudden drop caused a number of stocks, such as Accenture, to plummet, while others, such as Apple and Hewlett-Packard, experienced huge spikes.

A subsequent report by the SEC revealed that many algorithmic trading programs were the cause of the market’s sudden drop. As these programs withdrew, liquidity evaporated and buyers disappeared. Trading was temporarily suspended, and when it resumed, buyers took advantage of the market and prices bounced back quickly. The NYSE and NASDAQ cancelled trades executed more than 60% away from the opening price of the day.

In response to this event, the SEC approved a rule to halt trading for five minutes in stocks that experience a rise or fall of more than 10% in a five-minute period. This is intended to prevent algorithmic trading from rapidly moving share prices before human traders have a chance to determine if the changes are due to fundamental information.

-

Globalization of Stock Markets

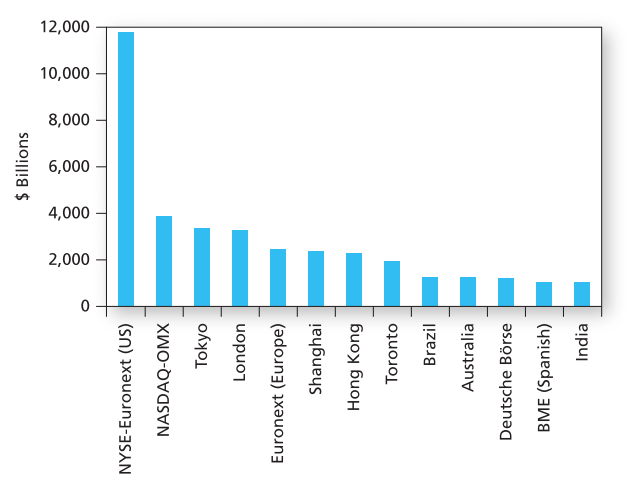

NYSE-Euronext is the largest equity market as measured by total market value of listed firms.

The securities market is facing pressure to form international alliances or mergers due to the rise of electronic trading. Traders view stock markets as computer networks that connect them to other traders, allowing them to trade a wider range of securities from around the world.

To stay competitive, it is crucial to have efficient and cost-effective mechanisms for executing and clearing trades.

-

In the US:

- The NYSE merged with Archipelago ECN in 2006 and acquired the American Stock Exchange in 2008.

- NASDAQ acquired Instinet in 2005 and the Boston Stock Exchange in 2007.

- In the derivative market, the Chicago Mercantile Exchange acquired the Chicago Board of Trade in 2007 and the New York Mercantile Exchange in 2008.

-

In Europe:

- Euronext was formed through the merger of the Paris, Brussels, Lisbon, and Amsterdam exchanges, and later purchased Liffe, a derivatives exchange based in London.

- The London Stock Exchange merged with Borsa Italiana, which operates the Milan exchange, in 2007.

-

-

Intercontinental:

- The NYSE Group and Euronext merged in 2007.

- In 2011, Deutsche Borse and NYSE Euronext announced their intention to merge, but the proposed merger fell through in early 2012 after European Union antitrust regulators recommended blocking the combination.

- The NYSE and the Tokyo Stock Exchange have announced plans to link their networks, giving their customers access to both markets.

- NASDAQ Stock Market merged with OMX, which operates Nordic and Baltic stock exchanges, in 2007 to form NASDAQ OMX.

- In 2008, Eurex acquired International Securities Exchange (ISE) to form a major options exchange.

-

Trading Costs

When trading securities, there is always a fee involved, which is paid to the broker. There are two types of brokers: full-service and discount brokers.

-

Full-service brokers offer a range of services and are often referred to as account executives or financial consultants. In addition to executing orders, holding securities for safekeeping, offering margin loans, and facilitating short sales, they also provide investment information and advice. These brokers have a research team that prepares analysis and forecasts of general economics, industry, and company conditions, and makes specific buy or sell recommendations. Some customers establish discretionary accounts, which allow the broker to make buy and sell decisions on their behalf. However, this requires a high level of trust since the broker could execute trades solely for the purpose of commission.

-

Discount brokers, on the other hand, offer basic services such as buying and selling securities, holding them for safekeeping, offering margin loans, and facilitating short sales. They do not provide any additional information or advice, only price quotes. Many banks, thrift institutions, and mutual fund management companies now offer these services. Some discount brokers, such as Schwab, E*Trade, or TD Ameritrade, now offer commissions below $10.

In addition to the explicit trading fee, which is the broker’s commission, there is also an implicit fee in the form of the dealer’s bid-ask spread. Some brokers may offer no commission, but instead collect their fee entirely in the form of the bid-ask spread.

-

-

Buying on Margin

Investors have the option to finance their securities purchases through a source of debt financing known as broker’s call loans or buying on margin. This means that the investor borrows part of the purchase price from a broker and only contributes a portion of the total cost, known as the margin. The broker then borrows the remaining amount from banks at a call money rate and charges their clients this rate, along with a service charge, for the loan.

All securities purchased on margin must be kept with the brokerage firm and serve as collateral for the loan. The Federal Reserve System regulates the extent to which stock purchases can be financed through margin loans, with the current requirement being that the investor must pay 50% of the purchase price in cash.

-

Example on Margin Call

The concept of percentage margin refers to the relationship between the equity value of an investment account and the market value of the securities it holds. It is calculated as the ratio of the net-worth of the account to the market value of the securities.

For example, if an investor pays $6,000 towards the purchase of $10,000 worth of stock (100 shares at $100 each), and borrows the remaining $4,000 from the broker, the initial percentage margin would be 60% ($6,000/$10,000).

However, if the stock price drops to $70 per share, the total value of the stock would be $7,000. With the loan from the broker still at $4,000, the investor’s equity would be $3,000 ($7,000 - $4,000), and the percentage margin would drop to 43% ($3,000/$7,000).

To avoid the situation where the stock value falls below the loan from the broker, resulting in a negative equity, brokers set a maintenance margin. This requires the investor to add new cash or securities to the account if the percentage margin falls below a certain level. If the investor does not act, the broker may sell securities from the account to restore the margin to an acceptable rate.

For instance, if the maintenance margin is 30%, the stock price can fall to $57.13 before the margin would fall below the required level.

-

Why to buy in Margin

Investors often buy securities on margin to invest more than their own money allows. This gives them the potential for greater upside, but also exposes them to greater downside risk.